What does it mean for the bear market in shares?

Key points

- Global share markets have fallen into a bear market, but whether this turns out to be long or short depends on how long the hit to the economy from coronavirus lasts.

- There are big differences between the current disruption to economic activity – which could be very deep in the short term - and past recessions and depressions.

Introduction

Global and Australian shares have fallen well beyond the 20% decline commonly used to delineate a bear market. From their highs to their recent lows major share markets have had roughly 35% falls as investors have moved to factor in a big hit to growth from coronavirus shutdowns.

Recession now looks inevitable and they tend to be associated with deep and long bear markets, but now there is even talk of depression suggesting an even deeper bear market. In reality, there are big differences now compared to past recessions and the Great Depression, so it really looks like an economic hit like no other with very different implications for the bear market in shares. But let’s first look at past bear markets as they provide some lessons for investors regardless of the cause.

The two bears - gummy & grizzly

There are 2 types of bear markets in shares:

- “gummy” bear markets with falls around 20% meeting the technical definition many apply for a bear market but where a year after falling 20% the market is up (like in 1998 in the US, 2011 and 2015-16 for Australian & global shares); and

- “grizzly” bear markets where falls are a lot deeper and usually longer lived (like in 1973-74, US and global shares through the tech wreck or the GFC).

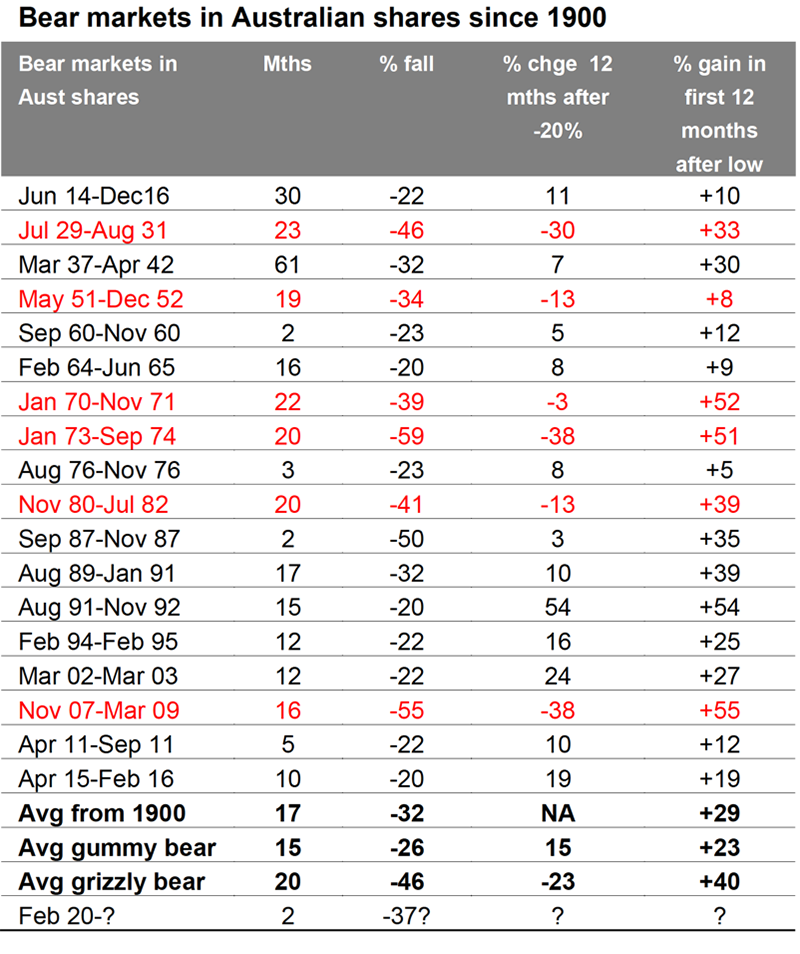

I can’t claim the terms “gummy bear” and “grizzly bear” as I first saw them applied by stockbroker Credit Suisse a few years ago. But they are a good way to conceptualise bear markets. Grizzly bears maul investors but gummy bears eventually leave a nicer taste (like the lollies!). The next table takes a closer look at bear markets. It shows conventionally defined bear markets in Australian shares since 1900 – where a bear market is a 20% decline that is not fully reversed within 12 months. The first column shows bear markets, the second shows the duration of their falls and the third shows the size of the falls. The fourth shows the percentage change in share prices 12 months after the initial 20% decline. The final column shows the size of the rebound over the first 12 months from the low.

Based on the All Ords. I have defined a bear market as a 20% or greater fall in shares that is not fully reversed within 12 months. Source: Global Financial Data, Bloomberg, AMP Capital

Since 1900 there have been 12 gummy bear markets (in black) and six grizzly bears (in red). Several points stand out.

- First, gummy bear markets tend to be shorter & see smaller declines around 26% compared to 46% for the grizzly bears.

- Second, the average rally over 12 months after the initial 20% fall is 15% for the gummy bear markets but it’s a 23% decline for the grizzly bear markets.

- Third, the deeper grizzly bear markets are invariably associated with recession, whereas the milder gummy bear markets including the 1987 share market crash tend not to be. All the six grizzly bear markets, excepting that of 1951-52, saw either a US or Australian recession or both whereas less than half of the gummy bear markets saw recession. It’s also the case for the US share market.

- Finally, once the bear market ends the rebound is strong with an average gain of 29%. Trying to time this is hard with many who get out on the way down finding they don’t get back in until the market has risen above where they sold!

Recession versus depression or something else?

So, one of the key messages from history is that if we have a recession then the bear market will likely be grizzly and severe with markets even lower than they are today in 12 months’ time. It’s not necessarily that simple though as the shock this time is very different to those seen in the past. But first the bad news. Recession now looks inevitable. There is now even talk of “depression”. While there is a huge unknown around how long it will take to control the virus and hence how long the shutdowns will last it is looking clear that the short term hit to GDP will be deeper than anything seen in the post WW2 period hence the increasing references to the pre-war depression:

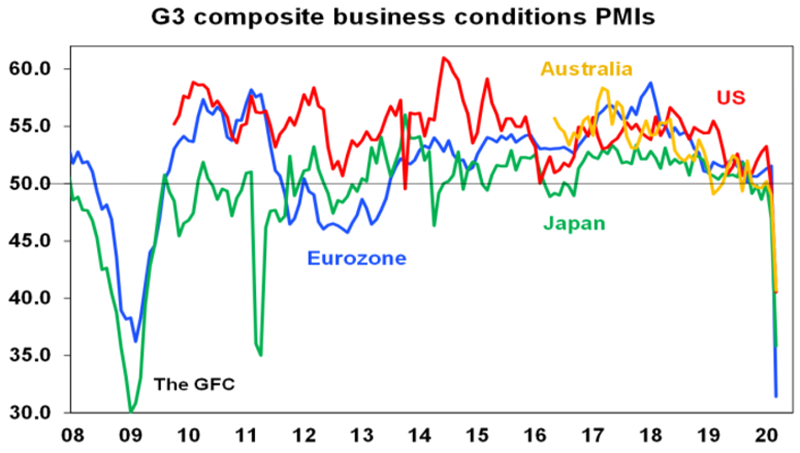

- Chinese business conditions PMIs for February fell an unprecedented 24 points due to shutdowns starting 23rd January. Consistent with this Chinese economic activity indicators are down 20% from levels a year ago. Chinese March quarter GDP could well be down 10% or so.

- Business conditions PMIs for the US, Eurozone, Japan and Australia all plunged in March as lockdowns ramped up. The average decline for these countries composite business conditions PMIs was an unprecedented 12 pts. This takes them below levels seen in the GFC. And the shutdowns have only just started so further falls are likely in April. So like China, developed countries could conceivably see 10% or so falls in GDP centred around the June quarter.

Source: Bloomberg, AMP Capital

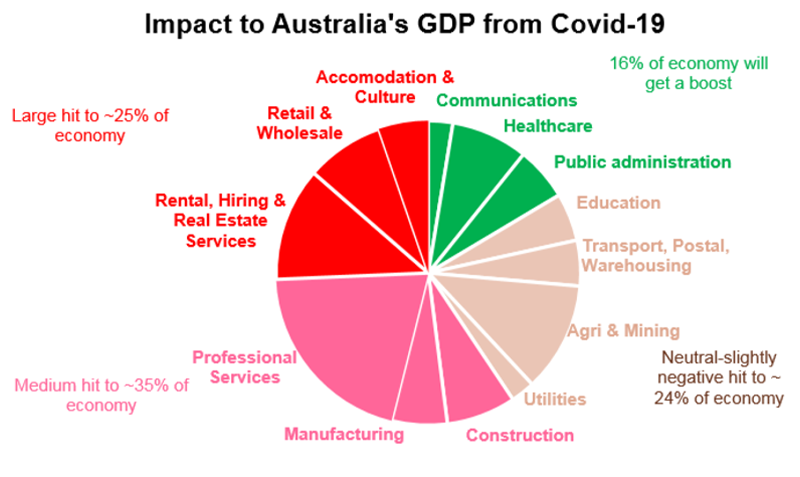

Source: ABS, AMP Capital

- By way of example the next chart shows the industry make-up of the Australian economy. The shutdowns will see a large hit to roughly 25% of the Australian economy, particularly accommodation & culture, retailing & real estate.

Big differences v past recessions and depressions

But while the slump in economic activity may be deeper than anything seen in the post war period, depression may not be the best description. Most definitions of depression focus on it being over several years and seeing a very deep fall in GDP compared to a recession which is shorter and shallower. The current hit to economic activity may be very deep but it won’t necessarily be longer than past recessions. And there is good reason to believe that if the virus comes under control in the next 2-6 months and we minimize the collateral damage from the shutdowns that the hit to activity may be shorter. There are big differences between the current situation and that of past recessions and Great Depression of the 1930s:

- First, recessions and The Great Depression (which saw GDP contract by 36% over 4 years and unemployment rise to 25% in the US and GDP fall by 9.4% in Australia with a rise in unemployment to 20%) were preceded by a period of excess in terms of investment, consumer discretionary spending, private debt growth and inflation that had to be unwound. This time around there has been no generalised period of excess and there has been no large-scale monetary tightening to bring on a downturn.

- Second, monetary policy was tightened in the lead up to past recessions and in the early phase of the Great Depression whereas global monetary policy was eased last year and that easing has accelerated this month with rate cuts, a renewed ramp up of quantitative easing (QE) and central banks around the world establishing various ways to ensure credit flows to the economy. In the 1930s banks were simply allowed to fail. Now they are being supported by ultra-cheap funding. Much of this owes to the GFC experience which has made it easier for central banks to now ramp up QE and introduce support mechanisms.

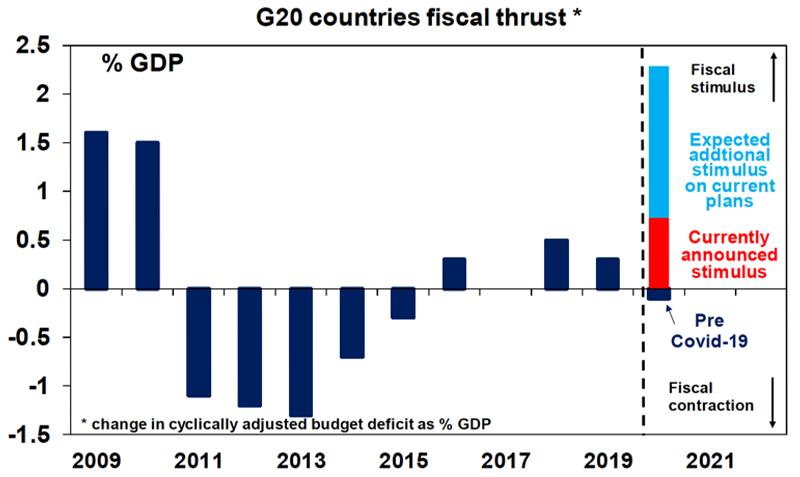

- Third, going into the Great Depression fiscal policy was tightened to balance budgets whereas in the last month we have seen massive and still growing global fiscal policy stimulus swamping that of the GFC. The latest US fiscal stimulus package alone is around 9% of US GDP.

Source: IMF, AMP Capital

- Fourth, there has been no trade war such as the Smoot-Hawley 20% tariffs on US imports that were met by global retaliation and saw global trade collapse in the 1930s.

The bottom line is that while we may see the biggest hit to global and Australian GDP since the 1930s thanks to the shutdowns, there are big differences compared to the Depression suggesting that a long drawn out global downturn is not inevitable. Basically, it’s a disruption to normal activity caused by the need to stay at home. In fact, growth could rebound quickly once the virus is under control and policy stimulus impacts. Which in turn should benefit share markets and could see this latest bear market turn into a gummy bear market rather than a grizzly bear market. Of course, at this point we are still waiting for convincing evidence that markets have bottomed. And the key is that the number of new cases of coronavirus starts to slow and that collateral damage from the shutdowns are kept to a minimum.

Closing Comment

Wow a lot can change in a short period of time!

In my last update I acknowledge there was a lot we did not know about this event and how it may play out. I finished with what we do know. After 31 years in Financial Planning

I have learnt that numbers and history do not lie, that’s why we are obsessed with numbers and graphs to illustrate, our conclusions.

I now ask you to re-read the table above, of what happened to the Australian Share market over the past 100 years when negative events occurred Globally, then look at the % gain in first 12 months after a low. Numbers don’t lie, nor history. Markets will recover, and when you’re sick you talk to the Medical Dr, when your financial affairs are sick talk to the Financial Dr. Now more than ever, you need to talk and review your situation to navigate out of here.

Please feel free to call us, we’re here to help you.

Bill and the team at SFP.

Remember we are available to help you during this unprecedented time...

If you have ANY please get in touch to speak with one of our Financial Planners we're here to help, either book a virtual meeting of get in contact with us on 02 9328 0876.

Article by Bill Bracey – Principal & Senior Financial Planner | Sydney Financial Planning

This article was prepared by Dr Shane Oliver. Dr Shane Oliver who provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.