Key points

- 2023 turned out to be a strong year for investors with shares and bonds rallying on the back of falling inflation, the anticipation of interest rate cuts in 2024 and better than feared economic growth. There were bumps along the way, but balanced super funds returned around 9.5%.

- 2024 is likely to see positive returns helped by falling rates but they are likely to be more constrained and volatile given risks around the timing of rate cuts, recession risks and geopolitics. The risk of recession in Australia is around 40%.

- We expect the RBA to cut the cash rate later in the year and as such expect the ASX and balanced super funds to rise off the back of this. Australian residential property prices are likely to soften ahead of support from rate cuts.

- The key things to watch are: inflation and rates; the risk of recession; China; US politics; and the Australian consumer.

Introduction

Happy New Year, it’s the 35th year I’ve been sending this opening year economic outlook, each additional year of experience providing me greater perspective on how investment markets behave and what successful clients need to do to build wealth.

Simply put, clients need the right financial plan and strategy, holding only quality assets, coupled with the right Financial Planning firm who deliver on their promises, who coach you to ride the storms out and provide a yearly review to measure and acknowledge progress and reset for the following year.

This time last year, I warned clients to expect higher volatility, and we sure got that right! I also noted that once interest rates start to fall share markets will rebound, then later followed by the property market. Sounds easy, but you need to hold your nerve!

Now its slowly starting, these things take time to flow through, there is always volatility, but it will reduce in time. Those who don’t have a trusted financial planner to guide them through the cycles never seem to build wealth, as they continue to make terrible emotional financial decisions that destroys wealth.

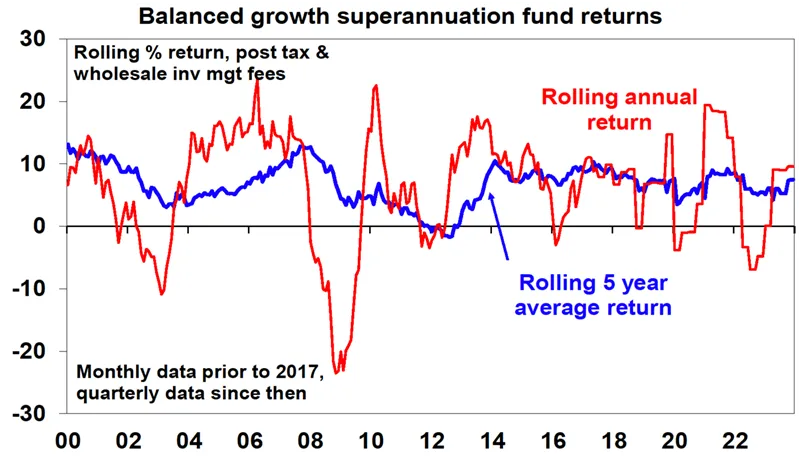

After poor returns in 2022 on the back of high and rising inflation, a surge in interest rates, the invasion of Ukraine and recession worries, 2023 was a far better year for investors as inflation fell and investment markets anticipated lower interest rates ahead. This saw average balanced growth superannuation funds return around 9.5% more than making up for the 4.8% loss in 2022, as both shares and bonds rallied. Over the last five years, they returned around 7.5% pa, which exceeded inflation.

Source: Mercer Investment Consulting, Morningstar, AMP

Can the rebound continue or will markets have a rough year? Here is a simple point form summary of key insights and views on the outlook.

Five key themes from 2023

- Stronger than feared growth. Despite fears recession was inevitable, on the back of rate hikes, it’s been avoided so far, helped by saving buffers, reopening boosts and some labour hoarding.

- Disinflation. Inflation across major countries fell from peaks of 8 to 11% in 2022 to around 3 to 5% as supply pressure and demand eased.

- Peak interest rates. Most major central bank policy rates look to have peaked and this probably includes the RBA’s cash rate.

- Geopolitical threats proved not to be as worrying as feared.

- Artificial intelligence hit the big time after the launch of Chat GPT. Thishelped tech stocks (mostly US) tech stocks reverse their 2022 slump.

Five lessons for investors from 2023

- Monetary policy still works in controlling inflation – the lags may be long and variable but this time was not really different. Of course, an easing in supply chain disruptions helped and there is still a way to go.

- Don’t ignore population growth – a surge in immigration played a big role in pushing home prices back up and avoiding recession in Australia.

- Timing markets is hard – it was easy to be gloomy a year ago with a long worry list and shares plunging into October but timing markets on the back of this was a loser as shares surged, putting in strong returns.

- Geopolitics matters – but it’s hard to predict (eg, Hamas’ attacks on Israel) and the impact can often be less than feared, with the world learning to live with the war in Ukraine and the Israel/Hamas war not (yet) causing a surge in oil prices.

- Turn down the noise – investors are being hit with often irrelevant, low quality & conflicting information which boosts uncertainty. The key is to turn down the noise and stick to a long-term strategy.

The three big worries for 2024

- Inflation is still too high and its decline is likely to remain bumpy – so central banks could still have another hawkish turn and even if not there is a high risk that rate cuts may come later than markets expect.

- The risk of recession is high. It’s hard to see the biggest rate hiking cycle since the 1980s not having a major impact and the risks are already evident in tighter US lending standards, falling lending in Europe and stalling consumer spending in Australia. Risks around the Chinese economy and property sector also remain high.

- Geopolitical risk is high: with half the world’s population seeing elections including the US, EU & India; the US Government could have a shutdown starting 19 January & could have another divisive Biden v Trump presidential election; the result of Taiwan’s 13 January election could see an easing or an escalation of tensions with China depending who wins; the war in Ukraine is continuing; and there is a high risk the Israel/Hamas war could spread, threatening oil supplies, particularly with Iran’s proxy Houthi rebels disrupting Red Sea shipping.

Four reasons for optimism

- Inflation has eased sharply to around 3% in major industrial countries and around 5% in Australia and is likely to continue to fall as: supply chain pressures have eased; demand is cooling; and labour markets are easing. This includes in Australia which lagged US inflation on the way up and is just doing so again on the way down.

- We expect the ECB to start cutting rates in March, followed by the Fed and BoC in the June quarter. While there is still a high risk of one more hike in Australia in February, falling inflation should head this off so our base case is that the RBA has peaked ahead of rate cuts from June, taking the cash rate down to 3.6% by year end. Just as rate hikes were bad for shares in 2022, rate cuts should ultimately be positive.

- While recession is a high risk and markets are no longer priced for it, if it does occur it should be mild: most countries have not seen a spending boom that needs to be unwound; in Australia consumer spending, housing investment and business investment are not running at excessive levels relative to GDP; and Chinese growth is soft and property sector risks are high, but it’s likely to target roughly 5% GDP growth again and back this up with fiscal stimulus if need be.

- Finally, while there’s lots of geopolitical risks they may not turn out so badly: the US has a strong incentive to avoid an escalation in the Israel/Hamas war; the Ukraine war could turn into a frozen conflict; & elections won’t necessarily go in an adverse direction for markets. In relation to the US, the presidential election year normally sees average share returns and Trump could falter before the election.

Key views on markets for 2024

Easing inflation pressures, central banks moving to cut rates and prospects for stronger growth in 2025 should make for okay returns in 2024. However, with growth still slowing, shares historically tending to fall during the initial phase of rate cuts, a very high risk of recession and investors and share market valuations no longer positioned for recession, it’s likely to be a rougher and more constrained ride than in 2023. We expect balanced growth super funds to return positively and in line with benchmarks this year.

- Global shares are expected to return positively and in line with benchmarks. The first half could be rough as growth weakens, but shares should ultimately benefit from rate cuts and lower bond yields and the anticipation of stronger growth later in the year and in 2025.

- Australian shares are likely to outperform global shares, after underperforming in 2023 helped by somewhat more attractive valuations. A recession could threaten this though so it’s hard to have a strong view. Expect the ASX 200 to end 2024 well ahead of the start of the year.

- Bonds are likely to provide returns around running yield or a bit more, as inflation slows, and central banks cut rates.

- Unlisted commercial property returns are likely to be negative again due to the lagged impact of high bond yields & working from home.

- Australian home prices are likely to fall slightly as high rates hit demand & unemployment rises. The supply shortfall should prevent a sharper fall & expect a wide dispersion. Rate cuts will help later in the year.

- Cash and bank deposits are expected to provide returns of over 4%.

- A rising trend in the $A is likely taking it above $US0.70, due to a fall in the overvalued $US and the Fed cutting rates more than the RBA.

Five points on Bitcoin

- Bitcoin rose 157% through 2023.

- However, this followed a 64% fall in 2022, so it remains very volatile.

- It and other crypto currencies remain highly geared to US shares and expectations for interest rates - explaining its sharp fall in 2022 when shares fell and rates rose and rebound with shares in 2023.

- Bitcoin is yet to find a clear use (beyond as something to speculate in) making it very hard to value fundamentally – unlike, say, property which provides rents and shares which provide earnings. Recent gains owe partly to excitement around this year’s “halving” (in the amount of Bitcoin that miners receive) and anticipation of an exchange traded fund that can invest in Bitcoin - rather than developments in its use.

- There is value in blockchain technology (for decentralised finance, contracts, etc) which is positive for cryptocurrencies like Ethereum, but this is hard to value.

Five things to watch

- Inflation – if it fails to continue falling as we expect, central banks will be more hawkish than we are allowing for, risking deep recession.

- Recession – a mild recession should be manageable but a deep recession will mean significant downside in shares.

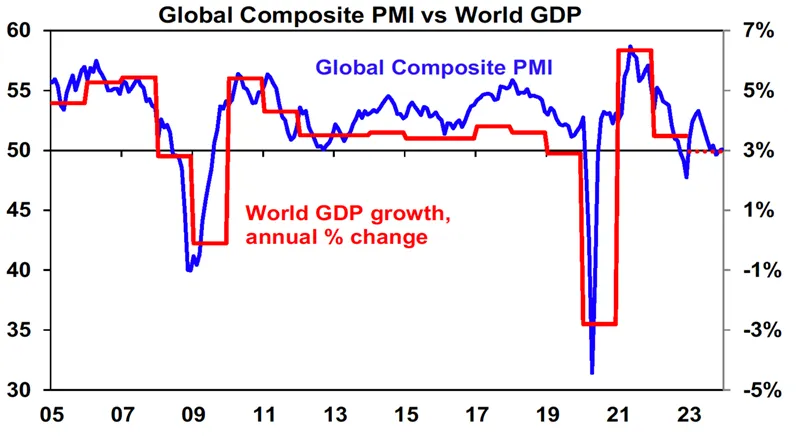

So far global business conditions PMIs are soft but consistent with okay growth.

Source: Bloomberg, IMF, AMP

- The Chinese economy – China’s property sector is continuing to struggle and without measures to support consumers this could hurt its economy with a flow on to demand for Australian exports.

- Geopolitics – the key risks relate to Taiwan, a possible expansion of the Israel/Hamas war and the US Presidential election.

- The Australian consumer – consumer spending has slowed sharply and risks stalling as a result of cost-of-living pressures, high interest rates and higher unemployment.

Nine things investors should remember

- Make the most of compound interest to grow wealth. Saving regularly in growth assets can grow wealth significantly over long periods.

- Using the “rule of 72”, it will take 16 years to double an asset’s value if it returns 4.5% pa (ie, 72/4.5) but only 9 yrs if the asset returns 8% pa.

- Don’t get thrown off by the cycle. Falls in asset markets can throw investors of a well-considered strategy, destroying potential wealth.

- Invest for the long-term. Given the difficulty in timing market moves, for most it’s best to get a long-term plan that suits your wealth, age and risk tolerance and stick to it.

- Diversify. Don’t put all your eggs in one basket.

- Turn down the noise. This is critical with the information overload coming from social and mainstream media, with plenty of clickbait.

- Buy low, sell high. The cheaper you buy an asset, the higher its prospective return will likely be and vice versa.

- Avoid the crowd at extremes. Don’t get sucked into euphoria or doom and gloom around an asset.

- Focus on investments you understand offering sustainable cash flow. If it looks dodgy, hard to understand or has to be justified by odd valuations or lots of debt, then stay away. There is no free lunch!

- Seek advice. Investing can get complicated and its often hard to stick to a long-term investment strategy on your own.

Closing Summary

So, in closing its remains critically important to continue to review your strategy every year, as everything in the world continues to change, you just may not be able to see it from where you are.

Make sure when we reach out to you via our new Calendly review booking system you lock in a meeting time.

Time will not stand still, nor will your wealth creation strategy needs.

Bill Bracey

CEO and Founder

Will your wealth creation strategy stand the test of time?

Speak with one of our Financial Planners about the best approach for your circumstances, either book a meeting or get in contact with us on 02 9328 0876.

This article was prepared by Dr Shane Oliver with opening and closing summary by William Bracey - CEO & Senior Financial Planner from Sydney Financial Planning. Dr Shane Oliver who provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Sydney Financial Planning Pty Ltd (ABN 29 606 413 254), trading as Sydney Financial Planning & Illawarra Financial Planning is an Authorised Representative & Credit Representative of Charter Financial Planning Limited, Australian Financial Services Licensee and Australian Credit Licensee.

This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. If you decide to purchase or vary a financial product, your financial adviser, and other companies within the AMP Group may receive fees and other benefits. The fees will be a dollar amount and/or a percentage of either the premium you pay or the value of your investments. Please contact us if you want more information. If you no longer wish to receive direct marketing from us you may opt out by contacting Sydney Financial Planning . You may still receive direct marketing from AMP as a product issuer, bringing to your attention products, offerings or other information that may be relevant to you. If you no longer wish to receive this information you may opt out by contacting AMP on 1300 157 173.