Below are the average super balances for different age groups in Australia so you can see how your super savings compare.

A healthy super balance can be a key ingredient in being able to live the life we want in retirement. But for many people, retirement is a long way off, and it can be hard to know if your super is on track. If you’ve been asking yourself – how much super should I have at my age? – read on to find out.

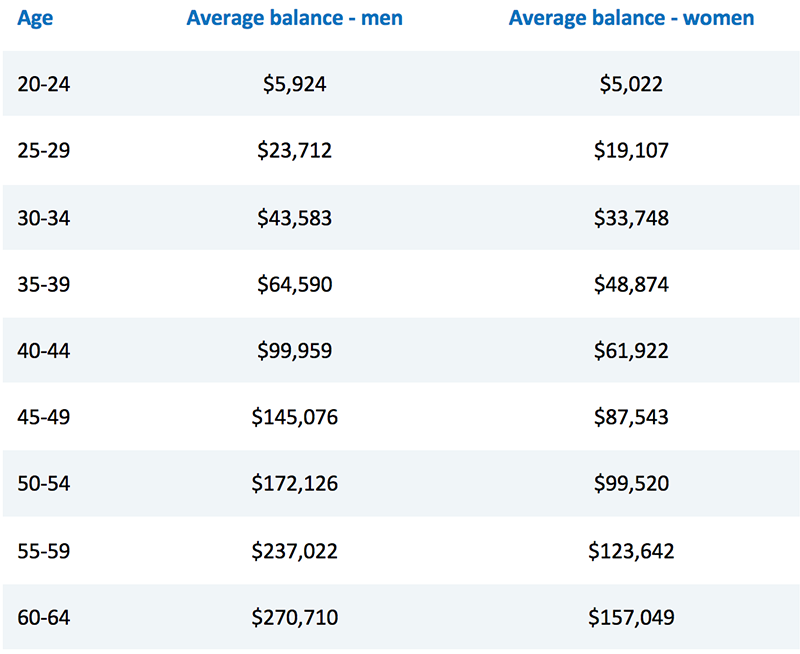

How does your super compare?

The table below shows the average super balances for Australian men and women of different ages (excluding those with no super) so you can compare your balance to others your age.

Source: Association of Superannuation Funds of Australia, Superannuation account balances by age and gender 2015-16, October 2017, pg. 9.

Does your super stack up?

If your balance looks low, there could be a number of reasons why your super is lagging your peers, such as taking time out of the workforce to study, travel, raise children, care for older relatives, or being out of work, working part-time, or earning a lower wage than others your age.

As the figures show, these issues particularly affect women, as they have lower super balances than men across all age groups.

Will your super be enough to retire on?

Even if your balance is above others of your age, will it be enough for a comfortable retirement?

The Association of Superannuation Funds of Australia (ASFA) says that “many people will still retire with inadequate superannuation savings to fund the lifestyle they want in retirement” and that “most people retiring in the next few years will rely partially or substantially on the Age Pension for some or all of their retirement as they have inadequate super savings”.1

The ASFA Retirement Standard estimates singles will need retirement savings of $545,000 for a comfortable retirement, while couples will need combined retirement savings of $640,000.2

These are lump sums required for a comfortable retirement assuming that the retiree/s will draw down all their capital and receive a part Age Pension. This simply means that the above balances will run out of money at average life expectancy (while people are still dependent on government benefits!!!)

This raises two important questions:

1. What if you (or one of you if you have a partner) will live longer than the average person?

In order to have $60,000 of annual reliable passive income (required by an average couple in NSW to live a comfortable lifestyle5) for life, our estimates show a couple would need approximately $1,340,000 of savings in total.6

2. What if your expenses are different to those of the average people?

Averages quoted by ASFA are great to start a good and relevant discussion. The next step would be work on your own individual retirement budget. Everyone’s circumstances are different, everyone’s retirement plan will look different. What will yours look like? What’s your personal retirement number?

Ways to boost your super

- Firstly, search for lost super. Money belonging to you might be sitting in an account you've forgotten about.

- Secondly, if you have super with multiple funds, think about consolidating them into one account and you could save on fees and charges that could be eating into your balance. However, you’ll need to check for exit or termination fees, and ensure that your insurance cover isn’t affected.

- And thirdly, you could consider changing how your super is invested, for example, by switching it into a more growth-focused investment option. Just bear in mind that returns are not guaranteed and that a big part of successful investing is about understanding what you own in your portfolio and why. To change your investment option, contact your planner.

Once you've got your super sorted with these quick wins, you can consider ways to boost your balance, including:

- Salary sacrificing: you can contribute extra cash into your super from your before-tax salary and it will only be taxed at 15%3, rather than at your usual marginal tax rate. However, make sure your total super contributions (including any your employer makes on your behalf) don’t exceed $25,000 per year. One of the best way to reduce tax if you’re an employee.

- Personal tax-deductible contributions: if your employer doesn’t offer salary sacrifice, you’re unemployed, self-employed or don’t want to salary sacrifice, you can make a personal tax-deductible contribution to your super, which is also taxed at 15%, and subject to the $25,000 per year limit.

- After-tax contributions: (also known as non-concessional contributions): There’s a $100,000 limit per financial year on the amount of after-tax contributions you can make. If you are under age 65, you can also ‘bring forward’ the next two years’ worth of after-tax contributions and make up to $300,000 contribution in a financial year.4

- Spouse contributions: if your partner is out of work, a stay-at-home parent, working part-time or earning less than $40,000, adding to their super could benefit you both financially.

- Contribution splitting: you can split your super contributions between you and your partner. A great way to close the gender super gap.

- Government contributions: if you’re a low or middle-income earner, you may be eligible for contributions from the government or tax-offsets when you add after-tax money to your super.

Too many options? Need more help?

For more help and to ensure you're on track for a comfortable retirement, speak to your financial adviser at SFP. If you don't have an adviser, contact us on 02 9328 0876.

1 Association of Superannuation Funds of Australia, Superannuation account balances by age and gender 2015-16, October 2017, pg. 7.

2 Association of Superannuation Funds of Australia, ASFA Retirement Standard, pg. 4.

3 Or 30% if you earn $250,000 a year or more.

4 Providing your total super balance at 30 June 2017 is less than $1.4 million.

5 ASFA retirement standards – Detailed budget breakdown

6 SFP’s estimate of required funds in today’s dollars, assuming a withdrawal rate of 4.5% pa, and income returns of 5% pa.

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.

Photo by Nick Fewings on Unsplash