Key points

- Share markets have fallen sharply over the last week or so on the back of coronavirus concerns.

- Shares may still have more downside and the uncertainty around the coronavirus crisis is very high, but we are of the view that it’s just another correction.

- Key things for investors to bear in mind are that: corrections are normal; in the absence of recession, a deep bear market is unlikely; selling shares after a fall locks in a loss; share pullbacks provide opportunities for investors to buy them more cheaply; while shares may have fallen, dividends are smoother; and finally, to avoid getting thrown off a long-term investment strategy it’s best to turn down the noise during times like this.

Introduction

The plunge in share markets over the last week has generated much coverage and consternation. This is understandable given the rapidity of the falls – with US shares having their fastest 10% fall from an all-time high on record - and the uncertainty around the coronavirus (Covid-19) and its impact on economic activity. From their highs to recent lows US shares have fallen 13%, Eurozone shares have fallen 16%, Japanese and Chinese shares have fallen 12% and Australian shares have fallen 12%. This note looks at the issues for investors and puts the falls into context.

What’s driving the latest plunge?

The plunge basically reflects two things.

- After very strong gains from their last greater than 5% correction into August last year, share markets had become vulnerable to a correction.

- The uncertainty around the impact of the coronavirus outbreak which is on the verge of becoming a pandemic and its impact on global growth has unnerved investors dramatically. Shares had recovered from their initial fall on the back of the virus into early February on signs that the number of new cases in China was falling (which is continuing), limited cases outside China and expectations that policy easing would limit any damage. This has been blown apart in the last week as cases have popped up en masse in Italy, South Korea and Iran, more cases have appeared elsewhere around the world and this has resulted in expectations of a deeper and longer hit to global growth.

After big falls shares have become technically oversold, measures of negative investor sentiment such as the VIX (or fear) index and demand for option protection have spiked. So, shares could have a short-term bounce. But given the uncertainties around Covid-19 – with more cases in the US and Australia likely to pop up - the situation could get worse before it gets better, so the share pullback could have further to go - notwithstanding short-term bounces.

Considerations for investors

Sharp market falls with headlines screaming that billions of dollars have been wiped off the share market are stressful for investors as no one likes to see the value of their investments decline. The current situation is doubly stressful because of fears for our own and others health – particularly for the elderly. However, several things are worth bearing in mind:

First, while they all have different triggers and unfold a bit differently to each other, periodic corrections in share markets of the order of 5%, 15% and even 20% are healthy and normal. For example, during the tech/dot-com boom from 1995 to early 2000, the US share market had seven pull backs greater than 5% ranging from 6% up to 19% with an average decline of 10%. During the same period, the Australian share market had eight pullbacks ranging from 5% to 16% with an average fall of 8%. All against a backdrop of strong returns every year.

During the 2003 to 2007 bull market, the Australian share market had five 5% plus corrections ranging from 7% to 12%, again with strong positive returns every year. More recently, the Australian share market had a 10% pullback in 2012, an 11% fall in 2013 (the taper tantrum), an 8% fall in 2014, a 20% fall between April 2015 and February 2016, a 7% fall early in 2018, a 14% fall between August and December 2018 and a 7% fall into August last year. And this has all been in the context of a gradual rising trend. And it has been similar for global shares – with the last big fall in US shares being a 20% plunge into Christmas eve 2018. See the next chart. While they can be painful, share market corrections are healthy because they help limit a build-up in complacency and excessive risk taking.

Source: Bloomberg, AMP Capital

Source: Bloomberg, AMP Capital

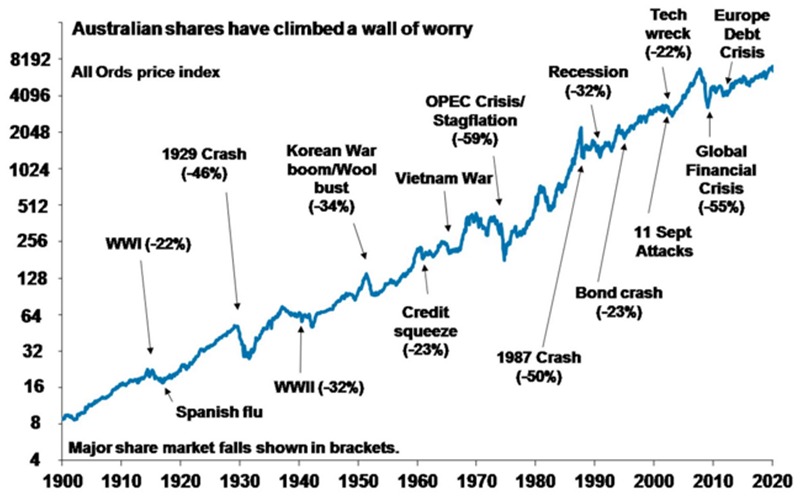

Related to this, shares climb a wall of worry over many years with numerous events dragging them down periodically, but with the long-term trend ultimately up & providing higher returns than other more stable assets. Bouts of volatility are the price we pay for the higher longer-term returns from shares.

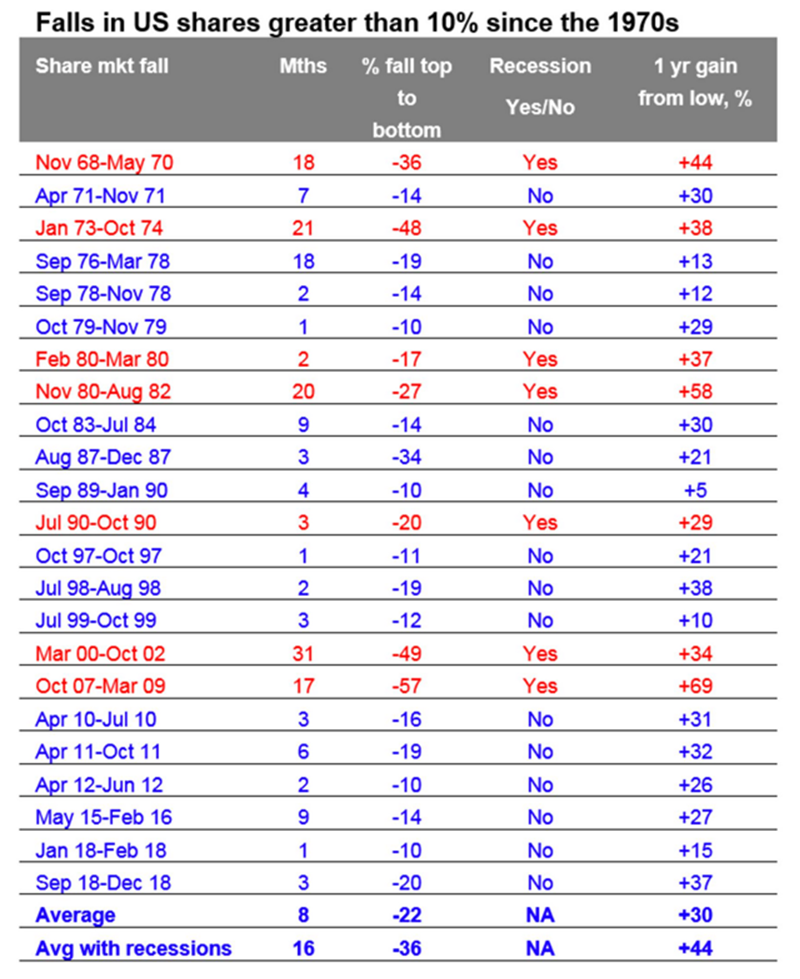

Second, the main driver of whether we see a correction (a fall of 5% to 15%) or even a mild bear market (with say a 20% decline that turns around relatively quickly like we saw in 2015-2016) as opposed to a major bear market (like that seen in the global financial crisis (GFC)) is whether we see a recession or not – notably in the US as the US share markets tends to lead for most major global markets. The next table shows US share market falls greater than 10% since the 1970s. I know it’s heavy – but I like this table! The first column shows the period of the fall, the second shows the decline in months, the third shows the percentage decline from top to bottom, the fourth shows whether the decline was associated with a recession or not and the fifth shows the gains in the share market one year after the low. Falls associated with recessions are highlighted in red.

Source: Bloomberg, AMP Capital

Several points stand out:

- First, share market falls associated with recession tend to be longer and deeper.

- Second, after the low the, share markets generally rebound sharply – which invariably makes it very hard for investors to time, as by the time they realise what has happened and get back in the market is above where they sold.

- Finally, as would be expected the share market rebound in the year after the low is much greater following falls associated with recession.

So, whether a recession is imminent or not in the US is critical in terms of whether we will see a major bear market or not. In fact, the same applies to Australian shares. Our assessment is that a US/global recession is not inevitable. We have not seen the excesses – in terms of overall debt growth (although housing debt is a source of risk in Australia), overinvestment, capacity constraints and inflation – that normally precede recessions in the US, globally or Australia. And we have not seen the sort of monetary tightening that leads into recession. In fact, monetary conditions remain very easy. However, the uncertainty around the coronavirus outbreak and the likelihood of economic shutdowns designed to contain it beyond those in China do suggest a greater than normal risk on this front. That said even if there were a recession growth would likely rebound quickly once the virus came under control as economic activity sprang back to normal helped by policy stimulus.

Third, selling shares or switching to a more conservative investment strategy or superannuation option after a major fall just locks in a loss. With all the talk of billions being wiped off the share market, it may be tempting to sell. But this just turns a paper loss into a real loss with no hope of recovering. The best way to guard against making a decision to sell on the basis of emotion after a sharp fall in markets (as many including me are tempted to do!) is to adopt a well thought out, long-term strategy and stick to it.

Fourth, when shares and growth assets fall, they are cheaper and offer higher long-term return prospects. So, the key is to look for opportunities the pullback provides – shares are cheaper and some more than others. It’s impossible to time the bottom but one way to do it is to average in over time.

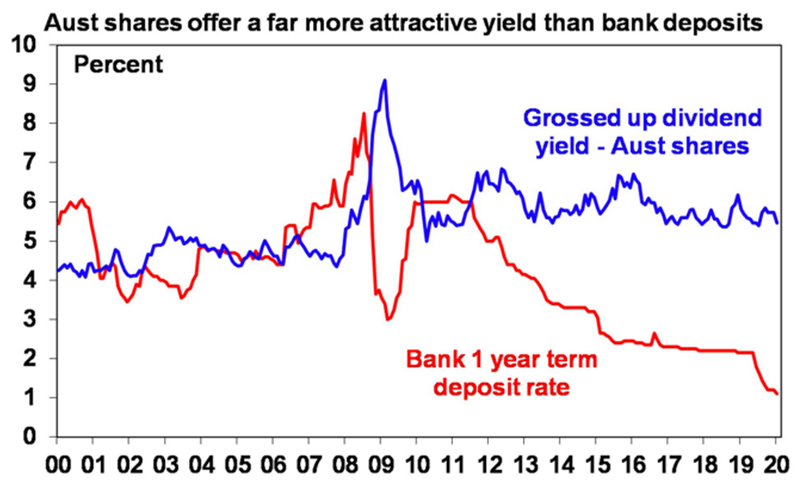

Fifth, while shares have fallen, dividends from the market haven’t. They will come under some pressure as the economy and profits take a hit from a deeper and longer coronavirus outbreak. But companies like to smooth their dividends over time – they never go up as much as earnings in the good times and so rarely fall as much in the bad times. So, the income flow you are receiving from a well-diversified portfolio of shares is likely to remain attractive, particularly against bank deposits.

Source: RBA, Bloomberg, AMP Capital

Sixth, shares and other related assets often bottom at the point of maximum bearishness, ie, just when you and everyone else feel most negative towards them. So, the trick is to buck the crowd. “Be fearful when others are greedy. Be greedy when others are fearful,” as Warren Buffett has said.

Finally, turn down the noise. At times like this, negative news reaches fever pitch. Talk of billions wiped off share markets and warnings of disaster help sell copy and generate clicks & views. But we are rarely told of the billions that market rebounds and the rising long-term trend in share prices adds to the share market. Moreover, they provide no perspective and only add to the sense of panic. All of this makes it harder to stick to an appropriate long-term strategy let alone see the opportunities that are thrown up. So best to turn down the noise.

Concluding Comment

So in summary as I suggested in January in my update to you, times like this offer opportunity and we have seen times like this before. This is where the rich get richer and the poor non advised, get poorer.

Please take time to watch my 5 minute video that explains what you should be doing with this market.

Now more than ever its important to keep your nerve and shut out the media who pump FEAR into the masses.

Please feel free to contact us at Sydney Financial Planning, we are experienced at dealing with volatile times and know what to do.

Bill Bracey and the team

Have you set things up to weather this trend?

If you need your personal situation reviewed by your SFP Planner or you don't have a planner yet, get in contact with us on 02 9328 0876.

Bill Bracey – Principal & Senior Financial Planner | Sydney Financial Planning

This article was prepared by Dr Shane Oliver. Dr Shane Oliver who provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.