Market corrections , market dips, bear markets..... who loves them? Not many...but what if I told you that maybe you should…?

Actually, they’re never called any of the above. They’re always called a crash.

The mainstream media loves a “crash”, but let’s think through what actually happens…

What I’d like you to get out of this blog post is to love market corrections … welcome them, see why they have to happen, how little they mean in the long run and how much advantage you have over them – if you only process them the right way.”

The difference between the mind of a victim and the mind of an opportunist

First of all, let’s start calling things by their real names.

A crash is something definite, irreversible. Planes crash … cars crash. Markets don’t crash… markets correct. Their permanent growth is randomly interrupted by temporary declines. (Please notice the use of the adjective temporary). These happen often for no apparent reason, we can’t predict exactly when they happen and why? And guess what?! We don’t have to.

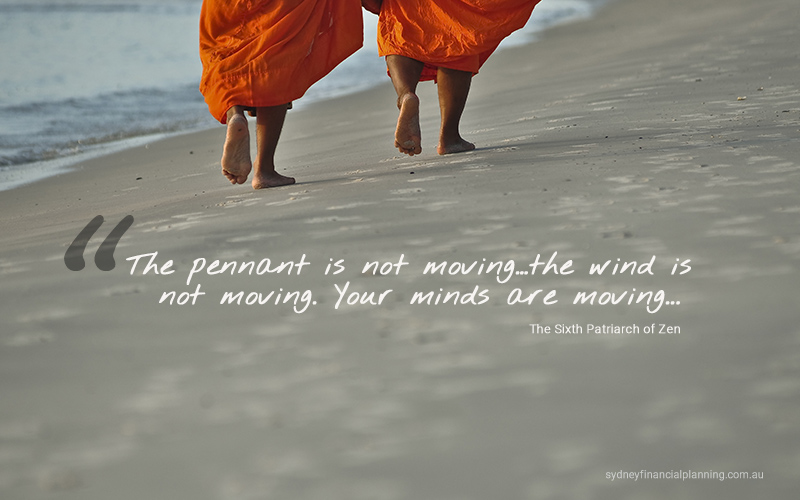

Let me tell you a story...There is an old Zen parable that speaks of two monks; sitting on a hill, watching a flapping pennant in the wind.

The first monk says: ‘The pennant is moving, the wind is not moving’.

The other monk says: ‘No, it’s the wind that is moving, the pennant is not moving’.

A third monk happens to walk by and he overhears the conversation. He turns his head and says to his friends: ‘The pennant is not moving…the wind is not moving. Your minds are moving....’

This parable precisely describes what happens during a market correction.

You see, what actually happens in the market itself is infinitely less important than the following two things:

‘How surprised people get’ and ‘What they think is going on’.

And although the market correction is not predictable or controllable in any scientific way, these two things influence the way your ‘mind moves’ and are both totally predictable and controllable and I will argue also avoidable.

1. The element of surprise

It wasn’t that the market went down 50% between 2008 and 2009 that mattered. What really mattered was how it surprised many… how unprepared and shocked many people were when it happened.

We, humans, love fairy tales. When we experience good time, we want it to last. Sometimes, we want it so badly, that soon, we start believing that it’s not going to stop.

When we look at the events prior to the GFC (or the Great Panic), a few years of consistent and smooth double digit returns in the market, we simply slipped into this state of a false comfort. The minute you bought into this fiction of the ‘new era’ and you presumed that the market would only go up from that point onwards, there was no way you’d be ready for the market to come down 50%.

Of course, the market didn’t go down any more or less for you than it did for anybody else. The difference was – it caught you by surprise, which prevented you from dealing with it calmly, making sense of it all and having a ‘battle plan’ (which is largely a psychological battle plan) for waiting out the correction.

2. What do you think is going on?

It doesn’t matter how strong the wind is blowing and it doesn’t matter how much the pennant is flapping… What do YOU think is going on?

- If you think it’s the end of the world, you’re going to panic and sell.

- If you think, this time is different than the last correction and that it won’t go up again, you’re going to panic and sell again.

- If you think the market will just keep ‘crashing’ down, or it will take a hundred years for it to recover, you’re going to panic and sell!

- If you think that something so major happened in the economy that the market cycle has been repealed and the companies will stop making profits from now on, you’re going to panic and sell.

All this has nothing to do with the wind and it has nothing to do with the pennant…this is just ‘your mind moving’.

I think you might begin to understand by now, that rather than studying corrections, we should focus on how people process the idea of a correction (and from my perspective of a financial coach, how passionately they’re coached).

Simply because this is what’s going to make all the difference. These are all the behavioural variables and therefore are all variables under our control.

But you need to recognise it and your financial (investment) adviser needs to recognise it.

Otherwise, all will be lost.

Still have questions or concerns?

It can really help to seek the help of a professional to discuss the best investment strategies for you. Why not call us to arrange an appointment on 02 9328 0876.

Article by Michal Bodi | Senior Financial Planner

Photo by Brooke Lark on Unsplash

General Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.