Contributing some of your pre-tax salary, wages or a bonus into super could help you to reduce your tax and invest more for your retirement.

How does the strategy work?

With this strategy, known as salary sacrifice, you need to arrange for your employer to contribute some of your pre‑tax salary, wages or bonus directly into your super fund.

The amount you contribute will generally be taxed at the concessional rate of 15%1, not your marginal rate which could be up to 47%2. Depending on your circumstances, this strategy could reduce the tax you pay on your salary, wages or bonus by up to 32%.

Also, by paying less tax, you can make a larger after-tax investment for your retirement, as the case study on the opposite page illustrates.

What income can be salary sacrificed?

- You can only sacrifice income that relates to future employment and entitlements that have not been accrued.

- With salary and wages, the arrangement needs to be in place before you perform the work that entitles you to the salary or wages.

- With a bonus, the arrangement needs to be made before the bonus entitlement is determined.

- The arrangement, which should be documented and signed by you and your employer, should include details such as the amount to be sacrificed into super and the frequency of the contributions.

Other key considerations

- Salary sacrifice contributions count towards the ‘concessional contribution’ cap. This capis $27,500 in FY 2021/22, or may be higherif you didn’t contribute your full concessionalcontribution cap since 1 July 2018 and areeligible to make ‘catch-up’ contributions. Tax implications and penalties apply if you exceed your cap.

- You can’t access super until you meet certain conditions.

- Another way you may be able to grow your super tax-effectively is to make personal deductible contributions (see opposite page).

Seek advice

A financial adviser can help you determine whether salary sacrifice suits your needs and circumstances.

Case Study

William, aged 45, was recently promoted and has received a pay rise of $5,000, bringing his total salary to $90,000 pa.

He plans to retire in 20 years and wants to use his pay rise to boost his retirement savings..

After speaking to a financial adviser, he decides to sacrifice the extra $5,000 into super each year.

By using this strategy, he’ll save on tax and have an extra $975 in the first year to invest into super, when compared to receiving the $5,000 as after-tax salary (see Table 1).

If he continued to salary sacrifice this amount into super, this could lead to William having an additional $150,394 in his super after 20 years (see Table 2).

Table 1. After-tax income vs salary sacrifice

Details

|

Receive pay rise as after-tax salary

|

Sacrifice pay rise into super

|

|---|

| Personal super contribution |

$5,000 |

$5,000 |

| Less income tax at 34.5%3 |

($1,725) |

(N/A) |

| Less 15% contributions tax |

(N/A) |

($750) |

| Net amount |

$3,275 |

$4,250 |

| Additional amount in super |

21%2 |

$975 |

Table 2. Super balances4

Year

|

No salary sacrifice

|

Salary sacrifice into super

|

Difference

|

|---|

| Year 5 |

$279,725 |

$304,029 |

$24,304 |

| Year 10 |

$416,168 |

$472,072 |

$55,904 |

| Year 15 |

$593,558 |

$690,543 |

$96,985 |

| Year 20 |

$824,183 |

$974,577 |

$150,394 |

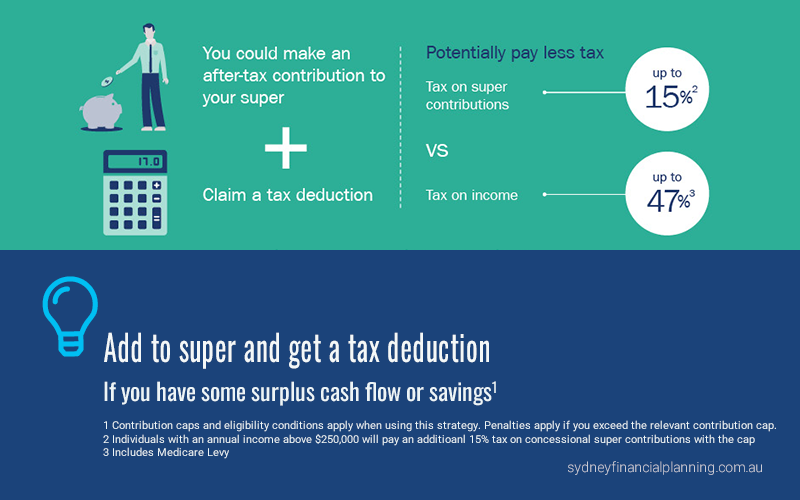

Personal Deductible Contributions

Like salary sacrifice, making a personal super contribution and claiming a tax deduction may enable you to boost your super tax-effectively. There are, however, a range of issues you should consider before deciding to use this strategy.

Your financial adviser can help you determine whether you should consider making personal deductible contributions instead of (or in addition to) salary sacrifice.

You may also want to ask your financial adviser for a copy of our super strategy card, called ‘Make tax-deductible super contributions’.

If you aren't sure how to proceed or if you meet the specific criteria...

Speak with one of our Financial Planners about the best approach for your circumstances asap, either book a meeting or get in contact with us on 02 9328 0876.

1 Individuals with income above $250,000 pa will pay an additional 15% tax on personal deductible and other concessional super contributions.

2 Includes Medicare Levy.

3 Includes Medicare Levy. Based on FY 2021/22 tax rates.

4 Assumptions: A 20-year comparison based on contribution of $5,000 pa of pre-tax salary on top of compulsory superannuation guarantee. Super investments earn a total return of 6.34% pa, balances shown at the end of 5/10/15/20 year periods. All figures are after income tax of 15% in super and capital gains tax (including discounting). These rates are assumed to remain constant over the investment period. William’s salary of $90,000 pa is indexed to CPI. Difference does not take into account money potentially invested outside super if pay rise received as after tax salary.

General Disclaimer: While every care has been taken in the preparation of this document, Sydney Financial Planning and Charter FP make no representations or warranties as to the accuracy or completeness of any statement in it.This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. Please seek personal financial advice prior to acting on this information.